The 17-Year Adoption Problem CMS Ignored

And the Model That Doesn't Need Traditional Health System At All

Several years ago, an innovation team at Harvard Pilgrim built a remote patient monitoring program for hypertension. It worked. Multiple clinical trials. Lives saved. Costs reduced. Evidence unimpeachable.

When they tried to scale it, it failed.

Not because the technology failed. Not because the evidence was wrong. It failed because when they asked physicians to adopt it, the physicians said something remarkable: “This might help bad doctors. My patients don’t need it.”

No villain. No incompetence. Just intelligent people whose deeply embedded beliefs about their own competence made the innovation invisible. Their mental structures — the frameworks through which they understood what good care looked like — prevented them from perceiving what the clinical data clearly showed.

This story is not about Harvard Pilgrim. It is about a structural reality that predates Harvard Pilgrim, that has persisted through every digital health innovation cycle since, and that the CMS ACCESS model — well-intentioned, directionally sound, and architecturally significant — is now about to encounter again.

It takes seventeen years for proven medical innovations to become standard clinical practice. Seventeen years. Most venture-backed digital health companies have a commercial runway of five years before they must show meaningful revenue. The companies that built durable businesses in digital health did so by finding a way to reach patients that did not depend on clinicians changing their behavior. The companies that failed — and the digital health graveyard is well-populated — tried to make the seventeen-year problem go away through better evidence, better education, better sales, or better payment.

ACCESS offers better payment. Payment is necessary. It is not sufficient.

Tuesday’s analysis established the rate comparison across three systems: the U.S. employer market, Germany’s DiGA program, and ACCESS. Today’s analysis examines why the rate gap is a symptom rather than the disease, what the architecture behind each model reveals about its underlying assumptions, and what a genuinely Creative response to Medicare’s digital health access problem would look like — one that harnesses what technology can now do, rather than asking technology to fit into structures designed before it existed.

Being right too early is indistinguishable from being wrong. The seventeen-year adoption problem isn’t a technology problem. It’s an identity problem.

Steel-Manning ACCESS: What It Gets Right

Before diagnosing ACCESS’s structural limitations, the framework requires presenting its strongest case — not to be polite, but because the strongest case reveals what the Creative response must preserve and build upon.

ACCESS gets several things genuinely right. First, it moves Medicare off activity-based payment and onto outcomes-based payment. That shift is foundational. Fee-for-service medicine has no mechanism for rewarding prevention, behavior change, or continuous engagement — precisely the things digital health does best. ACCESS creates a payment mechanism where those things are valued. That matters.

Second, ACCESS creates flexibility in care delivery that fee-for-service denies. Digital health tools, remote monitoring, non-physician care team members, and virtual coaching are all reimbursable under ACCESS in ways that Medicare’s traditional fee schedule does not accommodate. For a program covering 65 million Medicare beneficiaries, that flexibility is structurally significant.

Third, the scale of addressable population is real. James Pursley, President of Hinge Health, called the potential 30 million Medicare lives an “attractive long-term opportunity” — conditional on pricing, but genuine in scale. No employer market, however well-designed, reaches 30 million people with a single program structure.

Fourth, and most importantly for the long run, ACCESS creates a framework for evidence. CMS will publish annual standardized performance results for participating organizations. That transparency will, over time, separate high-performing platforms from low-performing ones in a way the current market — fragmented, employer-by-employer, opaque — cannot. For the digital health industry, that public evidence base is potentially more valuable than the payment rates.

These are the strongest arguments for ACCESS. They are real. They are worth preserving in any Creative redesign. The question is whether the current architecture can deliver on any of them — given the seventeen-year problem it has not yet solved.

The Structural Problem: Clinician Channel, Revisited

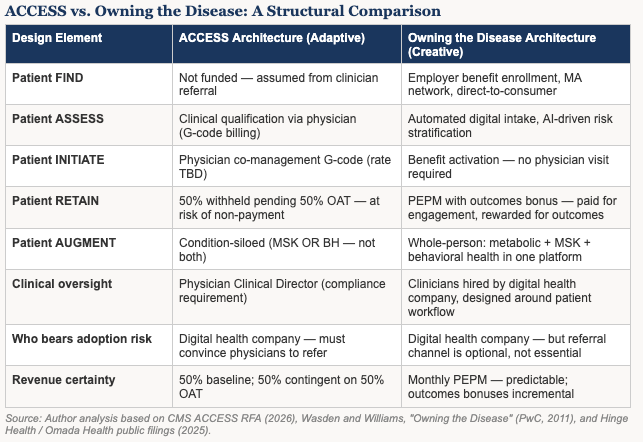

Access to the 30 million potential beneficiaries in ACCESS runs through a physician’s referral. The model allows for some direct patient outreach, and companies can market directly to Medicare beneficiaries. But the primary designed pathway is: physician identifies eligible patient, physician refers patient to participating digital health organization, physician co-manages patient to qualify for co-management G-codes, outcomes are tracked and reported.

The Harvard Pilgrim story illustrates what happens at the physician referral step. But it understates the problem, because it focuses on physician resistance as an attitude. The deeper issue is structural incentive misalignment. Consider what ACCESS asks a physician to do: identify an eligible patient from a complex panel of patients, learn about an available digital health program, make a referral that adds nothing to the physician’s reimbursement today, ensure co-management documentation to qualify for a G-code payment whose rate CMS has not yet published, and track an outcome that will be attributed to someone else’s platform.

Every one of these steps competes with the physician’s existing workflow. Time spent on ACCESS referrals is time not spent on billable procedures. The co-management G-code rate — theoretically available to compensate physicians for this coordination work — was not included in the February 2026 payment guidance. It was deferred to “later in 2026.” Physicians considering ACCESS participation are being asked to redesign their workflow around a payment rate that does not yet exist.

The Germany DiGA experience is instructive here. DiGA rates range from €180 to over €700 per 90-day prescription — annualized rates of $800 to $3,200, several times ACCESS levels. Germany’s statutory insurance system covers DiGAs as a mandated benefit, removing cost uncertainty from the patient equation. Even with these structural advantages, DiGA prescription rates remain well below projected levels. A 2024 study in rheumatology found 39.8% of patients were aware of DiGAs; only 12.6% had used one. A majority of German GPs have prescribed a DiGA at least once, but repeat prescribing — the behavior that drives scale — remains limited.

The lesson is not that Germany failed. The lesson is that even when the clinical channel is adequately funded and mandated, physician behavior changes slowly. Not because physicians are resistant to evidence. Because physicians are already operating at full capacity, and every new workflow competes with existing workflows. The adoption timeline does not compress because the payment rate improves. It compresses only when the physician’s role in the process is eliminated or radically simplified.

Owning the Disease: The Creative Architecture That Already Exists

In 2011, Chris Wasden and Brian Williams at PwC published a framework called Owning the Disease. The central argument was that the healthcare industry’s traditional model — selling products or services to clinicians who then deploy them to patients — was being structurally disrupted by the convergence of connected devices, behavioral data, and digital platforms. The companies that would win were those that reoriented their business model around the full patient journey: not just the transaction, but the continuum of finding patients early, assessing their needs, initiating engagement, retaining them over time, and augmenting their care as their needs evolved.

The paper described six design principles for what this model requires: continuous patient engagement, data integration across the care journey, technology that serves the patient rather than the clinician, outcomes accountability, scalable delivery infrastructure, and economic alignment between what companies are paid for and what patients need. The framework was written for a pharmaceutical industry beginning to confront biosimilar competition and chronic disease management demands. It turns out to have been a blueprint for digital health.

The companies that have demonstrated durable commercial success in digital health — Hinge Health, Omada Health, Spring Health, Lyra Health, Dario Health — built their platforms on Owning the Disease principles, whether or not they used that name. They found patients through employer benefit channels rather than clinician referrals. They assessed risk digitally rather than through physician diagnosis. They initiated engagement through benefit enrollment rather than clinic visits. They retained patients through behavioral science, personalized coaching, and continuous connected care rather than through episodic clinical touchpoints. They augmented care not by condition, but by person — building whole-person platforms that address metabolic, musculoskeletal, and behavioral health as an integrated continuum.

The result is a radically different cost structure. Hinge Health reported 77% GAAP gross margins in 2024 and 83% adjusted gross margins in Q1 2025. AI reduced human care costs by 95%. The company serves 49% of the Fortune 100 without a single physician referral channel. Omada Health reached 831,000 members, 66% GAAP gross margins, and its first positive adjusted EBITDA quarter in Q3 2025 — again, without physician referral as the primary growth channel.

These are not outliers. They are the evidence base that Owning the Disease works at scale. The architecture that makes it work is incompatible with the architecture ACCESS is built on.

The Three Response Types in Action

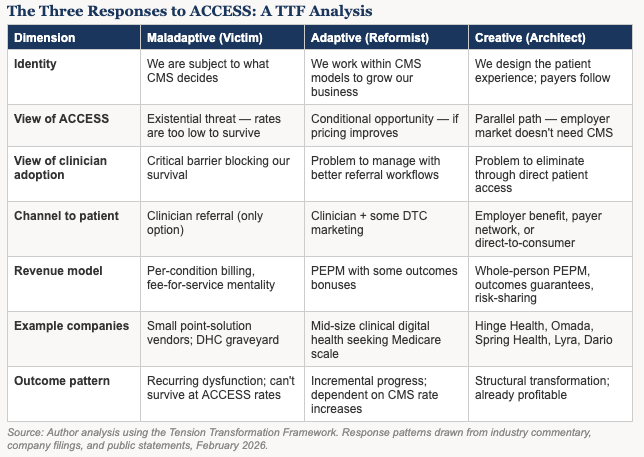

Tuesday’s analysis introduced three identity-based response patterns that appear whenever a major tension disrupts an industry. The ACCESS rate announcement has made those patterns visible in real time.

The Maladaptive response appears among smaller digital health companies that built point-solution models dependent on fee-for-service or employer-paid subscription revenue. For them, ACCESS rates represent existential math: $90 to $108 per year in probability-adjusted revenue for MSK or behavioral health cannot support the patient acquisition costs, compliance infrastructure, physician engagement costs, and clinical delivery costs required by the ACCESS architecture. These companies face the choice of sitting out ACCESS entirely or lobbying CMS for rate increases — seeking external intervention rather than redesigning their approach.

The Adaptive response appears among mid-size digital health companies that have the scale to potentially make ACCESS work but are treating participation as conditional on economics. Hinge Health President James Pursley said before rates were published that ACCESS would be a “2027 and beyond” story, contingent on pricing. Capstone analysts noted that large-scale companies could “trade near-term margin compression for greater scale” — an optimization framing, not a transformation framing. These companies are not threatened by ACCESS. They are assessing it as a growth channel with uncertain unit economics, and continuing to deepen the employer relationships that are already profitable.

The Creative response appears in a different place entirely. It appears among the employers, benefits advisors, and direct-to-patient platforms that have concluded the clinical channel is the wrong architecture regardless of payment rate — and built around it. Health Rosetta’s documented results — 20-55% cost reductions, improved outcomes, no clinician referral channel required — represent the Creative response at scale. So does the platform architecture that Hinge, Omada, Spring, and Lyra have built: clinicians hired to work within patient-centered workflows, not asked to refer into someone else’s platform.

The most significant Creative response, however, is emerging from an unexpected place: state-level AI policy.

Utah’s Architect Identity: What AI Makes Possible Now

In May 2024, Governor Spencer Cox signed SB149, creating the nation’s first state Office of Artificial Intelligence Policy. He appointed Dr. Zachary Boyd — a BYU mathematics professor specializing in machine learning and social science applications — as its director. The office opened with a specific mandate: not to regulate AI into compliance, but to enable responsible AI innovation through what it called a regulatory sandbox — a structured environment where companies can test novel AI applications with regulatory guidance rather than regulatory barriers.

The first healthcare participant in Utah’s AI sandbox was ElizaChat, an AI tool supporting teen mental health. The choice was deliberate. Utah faces one of the nation’s most acute behavioral health workforce shortages. In psychiatry, national supply projections suggest it would take twenty-seven years to balance clinician supply with demand. For teenagers in Utah needing mental health support, the clinical channel is not slow. It is largely absent.

Governor Cox’s framing of Utah’s AI strategy is worth quoting precisely: “AI is growing rapidly, and we are working to create an environment to ensure its growth and success while taking data privacy and security threats seriously.” By early 2026, Utah had three healthcare companies operating under regulatory mitigation agreements — including, notably, the first state-approved program allowing AI to legally participate in medical decision-making for prescription renewals. The 2025 National AI Readiness Index ranked Utah first among all fifty states. Salt Lake City was identified as the driving force.

What Utah’s AI sandbox makes visible is the economic transformation that AI enables in behavioral health — and why that transformation changes the math that ACCESS is trying to create.

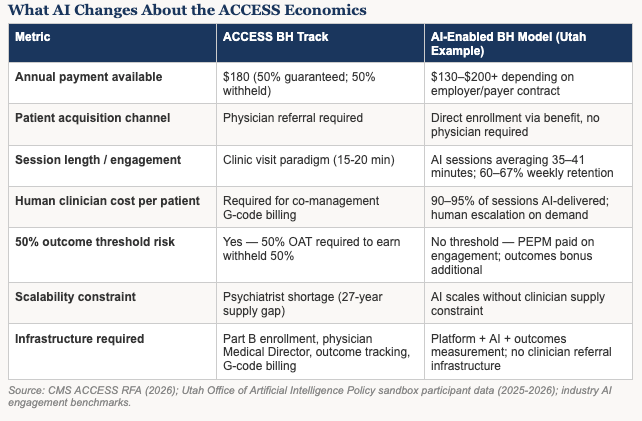

The traditional behavioral health delivery model is labor-constrained. Every patient interaction requires a licensed clinician. Reimbursement is tied to clinician time. Scale is capped by clinician supply. The ACCESS behavioral health track — $180 per year, 50% withheld — was designed for a world where behavioral health delivery costs are primarily clinical labor costs. That is the world that generated the 27-year supply gap. It is not the world that AI is creating.

AI-delivered behavioral health platforms have demonstrated something that changes the economic calculus entirely. One company in the Utah ecosystem achieved an average conversation length of thirty-five minutes with sixty percent weekly retention — double the industry baseline for digital health tools. An empathetic AI persona in a different platform averaged forty-one minutes per session with sixty-seven percent retention. These are not metrics from a clinical encounter. They are metrics from an AI-enabled therapeutic relationship that patients sustain by choice, not appointment.

The cost implications are significant. When 90-95% of therapeutic interaction is AI-delivered, the per-patient cost structure drops dramatically. Human clinicians escalate for complex cases, supervise AI interactions, and handle crisis response — but they are no longer the unit of production for every therapeutic touch. That changes what ACCESS-level rates can fund.

What a Creative Response to Medicare’s Digital Health Problem Would Look Like

The Creative response to the tension ACCESS is trying to address does not start with payment rates. It starts with architecture. Specifically, it starts by asking: which channel reaches the patient most reliably, at the lowest cost, with the highest retention? The data from the employer market and from AI-enabled behavioral health platforms points consistently in one direction: direct patient access, through benefit enrollment or direct-to-consumer engagement, with AI delivering the majority of therapeutic touch and human clinicians reserved for complex escalation.

A Creative architecture built on this foundation would look quite different from ACCESS. It would fund the FIND stage — the patient acquisition cost that ACCESS ignores entirely. The employer market funds FIND through benefit enrollment. DiGA funds it through physician prescription. ACCESS funds it through... nothing. Companies are expected to market to Medicare beneficiaries at their own expense, in a media environment dominated by Medicare Advantage plan advertising, against a population that does not identify as a digital health consumer.

It would separate the clinical oversight requirement from the patient acquisition requirement. ACCESS bundles them by design: the physician who refers is the physician who co-manages. A Creative architecture would allow digital health companies to provide clinical oversight through their own clinicians — as Hinge, Omada, and Spring already do in the employer market — without requiring that oversight to come through the patient’s primary care physician.

It would price around the whole person, not the condition. The ACCESS structure pays separately for MSK and BH — but 41% of patients with chronic pain have a co-occurring behavioral health condition. Treating these as separate tracks creates a perverse incentive to silo what good clinical practice integrates.

And it would let AI do what AI does best: sustain continuous therapeutic engagement between human touchpoints, at a cost structure that makes $180-420 per year viable rather than impossible. The Utah sandbox is demonstrating in real time that AI-enabled behavioral health can achieve retention rates that traditional digital health tools cannot, at a cost structure that reshapes what outcomes-based payment can fund. That is not a future possibility. It is a current reality that federal payment policy has not yet caught up to.

The Tension This Creates — And What It Means

ACCESS is not wrong. It is incomplete. The direction — outcomes-based payment, technology-enabled care, flexibility in delivery models — is precisely where Medicare needs to go. The evidence base that ACCESS will generate over time, by publishing annual performance results, will be genuinely valuable. The companies that participate and demonstrate results will be well-positioned as CMS iterates the model.

But the companies that are already building the Creative response — the Owning the Disease architecture, the employer-direct model, the AI-enabled engagement platform — are not waiting for CMS to get the payment rate right. They are demonstrating, in the employer market and in the Utah regulatory sandbox and in the international markets where outcomes-based digital health has run longer experiments, that the architecture works when the architecture routes around the seventeen-year problem.

The tension ACCESS has created is not primarily about rates. It is about identity. CMS is asking the digital health industry: do you want to be paid for delivering care the way Medicare has always paid for care — through physicians, in clinical settings, within established billing structures — or do you want to be paid for delivering care the way the patients need it delivered? The industry’s answer, from Hinge to Omada to Spring Health to DarioHealth to Health Rosetta’s network of self-insured employers, is already clear. The Creative architecture is already built. The question is whether federal payment policy will eventually catch up to what technology has already made possible.

Utah, under Governor Cox’s leadership, is not waiting for that question to be answered federally. It is running the experiment. That is federalism working as designed — and it is the strongest signal available of where the Creative response to Medicare’s digital health challenge is actually being built.

The companies that built durable businesses in digital health did not change the seventeen-year timeline. They found a way to reach patients that made the timeline irrelevant.

Endnotes

1. Wasden, Chris and Brian Williams. “Owning the Disease: The Strategic Value of Patient Support.” PwC Health Research Institute, 2011. The framework describes six levers of innovation and six design principles for companies that orient around the full patient journey rather than the point-of-care transaction.

2. Institute of Medicine. “Crossing the Quality Chasm: A New Health System for the 21st Century.” National Academies Press, 2001. The seventeen-year gap between evidence generation and standard clinical practice has been documented and replicated across multiple subsequent studies.

3. CMS, Advancing Chronic Care with Effective, Scalable Solutions (ACCESS) Model: Request for Applications and Supplemental Materials, December 2025 and February 2026. cms.gov/priorities/innovation/innovation-models/access

4. Hinge Health, Annual Report and Q1 2025 Earnings Call. investors.hingehealth.com. 77% GAAP gross margins FY2024; 83% adjusted Q1 2025; AI reduces human care costs by 95%; 49% Fortune 100 penetration.

5. Omada Health, Q3 2025 Earnings Call and SEC Filings. investors.omadahealth.com. 831,000 members; 66% GAAP gross margins Q3 2025; first positive adjusted EBITDA quarter.

6. Müller, S., et al. “Patient Awareness and Usage of Digital Health Applications in Rheumatology.” Journal of Medical Internet Research, 2024. 39.8% of rheumatology patients aware of DiGAs; 12.6% had used one.

7. GKV-SV DiGA Price Registry, June 2025. 44 permanently approved DiGAs; average 90-day prescription value €541. gkv-datenaustausch.de

8. Utah Department of Commerce. “Zachary Boyd Appointed as New Director of the Utah Office of Artificial Intelligence Policy.” April 2024. blog.commerce.utah.gov

9. Utah Office of Artificial Intelligence Policy. Annual Report 2025. ai.utah.gov/2025-2. Utah ranked #1 in DesignRush 2025 National AI Readiness Index. Three healthcare companies in regulatory sandbox by early 2026.

10. AI behavioral health engagement benchmarks: 35-41 minute average AI conversation length; 60-67% weekly retention rates cited from AI-enabled behavioral health platform performance data. Industry baseline for digital health tool retention: under 30% after week one (Rock Health, 2024 Digital Health Consumer Adoption Report).

11. American Association of Medical Colleges. “The Complexities of Physician Supply and Demand.” 2023. Psychiatry supply projection: 27-year timeline to balance supply with projected demand growth.

12. Capstone Partners. “ACCESS Model: Healthcare Technology Sector Analysis.” February 2026. Cited in Second Opinion Media coverage, February 13, 2026.

13. Dave Chase, Health Rosetta. healthrosetta.org. Documented case studies of self-insured employers achieving 20-55% healthcare cost reductions through Owning the Disease-aligned benefit redesign.

14. Business Group on Health. “2025 Large Employer Health Care Strategy Survey.” businessgrouphealth.org. 60% of large employers reassessing digital health vendor partnerships; movement toward whole-person platforms away from point solutions.